Alternative Liquidity Index, LP, a Delaware limited partnership (the “Purchaser”), today announced an offer to purchase up to 16,000 Multi-Strategy Series G Shares (the “Shares”), of Skybridge Multi-Adviser Hedge Fund Portfolios LLC (the “Fund”).

The Fund’s recent repurchase offer was oversubscribed, and this Offer provides an opportunity for investors to sell their entire investment for cash. This Offer is predicated upon the review and execution of appropriate transaction documentation.

The Purchaser is a Delaware Limited Partnership and is not affiliated with the Fund. The Offer is being made solely for the Purchaser to establish a passive ownership position in the Shares.

Investors should read the Offer to Purchase and the related materials carefully because they contain important information. Investors may obtain a free copy of the Offer to Purchase, and the Transfer Form by visiting their website at https://www.alternativeliquidity.net and clicking “Offers” or by calling Alternative Liquidity Capital at (888) 884-8796. Investors may also contact them at info@alternativeliquidity.net to answer questions about the Offer or to obtain Offer documents.

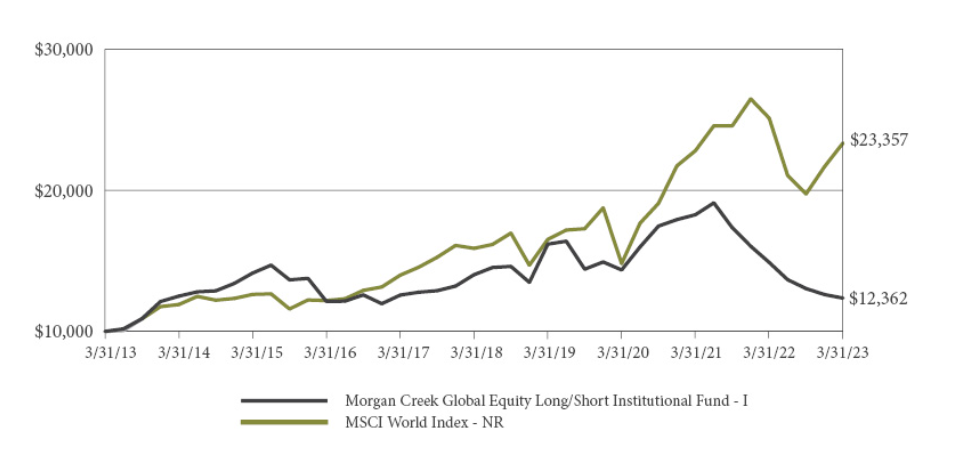

Morgan Creek Global Equity Long/Short Fund launched in 2011. It is an unlisted closed end fund(tender offer fund) that invests in a diversified portfolio of hedge funds and other private funds, mainly following long/short equity strategies, including both US and foreign stocks. They invested in many of the largest brand name hedge fund franchises including Tiger Global.

Unfortunately Morgan Creek had a difficult time in the mid to late 2010s. Its performance has lagged the MSCI World Index.

Morgan Creek Liquidation Plan

It faced a wave of redemption requests, making the funds operations uneconomical. Ultimately it decided to liquidate:

The asset size of the Fund had decreased to a level where the fixed operating costs of continuing to manage the Fund were difficult to justify, and in light of poor recent performance at that time, we did not have confidence in our ability to raise sufficient new funds to reduce the expense ratio in a timely manner. The Fund officially commenced its liquidation after the 2022 fiscal year audit was complete and the first distribution was paid in the middle of August.

Morgan Creek has already sold its most liquid assets, and made several significant distributions. In August 2022, they paid out approximately 48% of the fund’s June 30 NAV. During the second quarter of 2023, they paid out another 10%. The remaining portfolio consists of the most illiquid, difficult to sell assets.

The remaining portfolio consists of two managers, private holdings, and a cash balance to cover the Fund’s projected operating expenses. For the two remaining managers, Teng Yue provides 15% liquidity per quarter and Tiger Global 25% per year. We expect the final tranche of our full redemption in Teng Yue to process on March 31, 2024 and the final tranche of our full redemption in Tiger Global on December 31, 2024. The private holdings have no pre-determined liquidity schedule and we continue to evaluate all available liquidity options in the context of value maximization.

For the remaining assets, valuation is also a concern. Tiger Global made a lot of extremely aggressive investments in tech startups at extremely high valuations. In recent months they have been in the headlines as they struggle to find liquidity. It seems there is a high risk Tiger Global’s portfolio will be written down further, and the ultimate payout to investors will be far lower than the stated NAV. That will reduce the payout to investors in Morgan Creek Global Equity Long/Short Fund. At the same time, investors have limited visibility into the valuation methods of the other remaining portfolio holdings.

What if they are unable to sell the remaining assets? The plan of liquidation permits the Fund to establish a liquidating trust, and transfer remaining unsold assets into it. Fund investors would then be left holding liquidating trust units for an indefinite period of time.

No Exit?

As investors wait for Morgan Creek to liquidate the rest of the portfolio, they have few ways to get liquidity. The shares are not traded on any exchange. Morgan Creek had typically provided investors with liquidity through quarterly share repurchases, but they suspended all share repurchases since April 2022.

Investors who don’t want the uncertainty of the liquidation can try to sell their shares in a private transaction. Alternative Liquidity Capital recently launched a tender offer to buy a limited number of shares in Morgan Creek Global Equity Long/Short Fund. Investors with questions about the offer can find more information on Alternative Liquidity’s website.

SkyBridge is a famous, some would say infamous alternative asset manager. It is one of the largest sponsors of hedge fund vehicles that use the transparent 40 act fund structure known as a tender offer fund. SkyBridge Multi Adviser Hedge Fund Portfolios and SkyBridge G II Fund LLC each offer exposure to some of the top brand name hedge fund managers including Third Point and Point72. Both funds also have significant crypto exposure.

SkyBridge Tender Offers Oversubscribed

However, in recent months SkyBridge’s tender offer funds have faced a liquidity crunch. The most recent repurchase offers for SkyBridge’s tender offer funds were wildly oversubscribed. SkyBridge Multi Adviser Hedge Fund Portfolios repurchased just 8% of tendered shares in the most recent tender offer, as indicated in a May 12 filing. SkyBridge G II Fund repurchased just 11% of tendered shares according to a May 12 filing. Note that according to the prospectus for each fund, any repurchase plans are at the discretion of each fund’s respective board of directors.

This is the third time in three years that SkyBridge has faced major redemption requests, according to a recent Citywire article. In 2020, they were also faced with nearly $1 billion in redemption requests following a period of poor performance, and sell recommendations from analysts at Merrill Lynch and Citi.

FTX Bankruptcy Limbo

Anthony Scaramucci, the founder of SkyBridge, is no stranger to controversy. Six months ago, Sam Bankman Fried’s crypto exchange, FTX, bought 30% of SkyBridge Capital. Now Bankman-Fried potentially faces decades in prison for fraud and money laundering. FTX’s minority stake in SkyBridge is in “bankruptcy limbo.” SkyBridge Multi-Adviser Hedge Fund Portfolios also owns common and preferred stock in FTX Trading Ltd, although these investments were marked at zero in the latest portfolio disclosure.

Liquidity for SkyBridge Investors

Investors that hang on to their shares may very well be rewarded with long term outperformance. Scaramucci also told Citywire that their Series G fund is having their best year since 2012. However, some investors may be concerned with headline risk from the FTX bankruptcy, or need liquidity as soon as possible. Unfortunately, they face limited options, because there is no active secondary market for interests in any of SkyBridge’s funds. According to the prospectus for each fund, manager approval is required for any transfer between investors.

In certain circumstances, Alternative Liquidity Capital will consider purchasing interests in SkyBridge Multi-Adviser Hedge Fund Portfolios and SkyBridge G II Fund LLC. Please visit Alternative Liquidity Capital’s website, or email info@alternativeliquidity.net for more information.

Funds of hedge funds have no shortage of critics. The common concern that analysts have about funds of funds is the extra layer of fees. Hedge funds already charge high fees. Adding a funds of funds manager on top increases the return hurdle necessary to beat the market. Some people are skeptical that funds of hedge funds add any value when compared to a randomly selected group of hedge funds. There is a wide dispersion in performance among hedge funds. Do funds of funds help you gain access to the best opportunities?

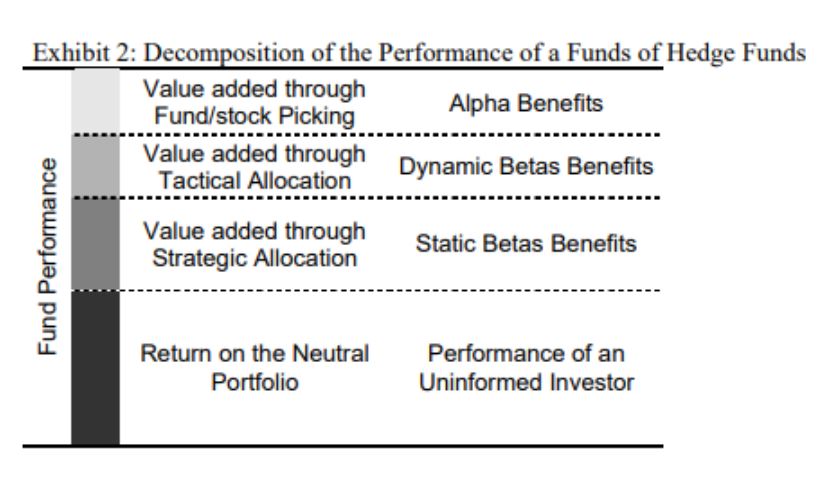

Researchers have studied this very question and identified three different ways that funds of funds managers can add value. First strategic allocation can provide static beta benefits. Second, tactical allocation can add dynamic beta benefits. Finally, fund selection can add alpha to a hedge fund portfolio.

This graphic demonstrates how Strategic Asset Allocation, Tactical Asset Allocation,and Fund Selection add value beyond a random selection of hedge funds:

Let’s examine each of these value add approaches individually.

Strategic Asset Allocation

Strategic asset allocation of a fund of hedge funds reflects the long-term bets made by the portfolio manager. Strategic asset allocation is a crucial step in the investment process. It adds the most value over the long term. Perhaps more importantly, it also builds resilience in the portfolio that will pay off when investors need it most. With proper strategic asset allocation, a hedge fund investor can get through a downturn while avoiding large losses.

Research from the EDHEC Risk Institute found statistically significant evidence of value add from strategic asset allocation under stressed market conditions from 2007-2009. The top 7.77% of hedge funds were able to add 3.50% annually.

Tactical Asset Allocation

While fund managers only rarely make strategic asset allocation shifts, they might frequently make tactical allocation shifts. Unfortunately, there is little evidence that most funds of hedge funds managers add value through tactical asset allocation. There are exceptions, however. Some managers are able to identify short term trends, and access the funds most capable of exploiting those trends.

Fund Selection

One barrier to hedge fund investing for firms with smaller staffs is the due diligence requirements. Consequently, they might turn to a fund of funds manager to help with due diligence on individual hedge funds. Indeed, fund selection is where its possible to truly add alpha.

However, Alternative Investments: An Allocators Approach notes that fund selection is a “double edged sword”. In normal markets, ~93% of fund of hedge funds had an annual positive outperformance of 3.9% over the neutral portfolio. However in stressed market conditions, only 48.4% of funds of hedge funds added value of 4.18% annually.

So ultimately, an allocator can benefit from a funds of funds approach. However, they need to make sure to find the right funds of hedge funds manager.

One way investors can access funds of funds in a transparent, tax friendly vehicle, is through unlisted closed end funds. To learn more about unlisted closed end funds pursuing hedge fund strategies, visit Tender Offer Funds.

The year started off with major news in the alternative investment and cryptocurrency industries. On January 4 SkyBridge LP announced the launch of SkyBridge Bitcoin Fund LP. The purpose of this fund is to provide mass-affluent investors with an institutional grade method of accessing Bitcoin.

SkyBridge released a whitepaper summarizing their bitcoin thesis in December 2020. Their reason for investing in Bitcoin is focused on macroeconomics, especially the impact of record money printing. Although these same macroeconomic reasons would typically lead one to invest in gold, Bitcoin does have several advantages compared to Gold.

We believe Bitcoin is in its early innings as an exciting new asset class,” said SkyBridge founder and managing partner Anthony Scaramucci. “With the institutional quality custody solutions available today, we believe the time is right to allocate capital and provide our clients access to the digital assets space.

Analysts have argued that growing institutional acceptance of Bitcoin is likely to be a major driver of upward price movement in digital assets. How will this ultimately play out? Perhaps history is a useful guide. Commodities were at one time considered a risque asset class. Once Wall Street built structured products tracking them, however, they became mainstream. In fact commodities are now considered essential in many asset allocation frameworks. Its likely Bitcoin will follow a similar path.

In recent years, entrepreneurs have developed custody and execution services to serve funds investing in bitcoin. As a result its becoming easier to set up a bitcoin focused fund. Private placements are an easy way to reach accredited investors. To reach a broader audience, closed end interval funds are a great option.

SkyBridge Bitcoin Fund Structure

SkyBridge Bitcoin Fund LP will charge a 0.75% annual management fee, and no incentive fee. According to to the Form D available on the SEC website, the minimum investment is $50,000. Hastings Capital Group LLC, will be involved in the sale and distribution of the Fund. Accredited investors can subscribe directly to the fund. SkyBridge is starting off with skin in the game- they will seed the the fund with $25.3 upon launch.

Although the SkyBridge Bitcoin Fund LP is focused exclusively on Bitcoin, SkyBridge will also be adding Bitcoin exposure to other funds. According to the press release, SkyBridge purchased $310 million in Bitcoin across its various flagship funds, as of the end of 2020.

More about SkyBridge

SkyBridge is global alternative investment manager that provides a range of investment solutions to individuals and institutions. Addressing every type of market participant, SkyBridge’s investment offerings include commingled funds of hedge funds products, customized separate account portfolios, hedge fund advisory services, and an Opportunity Zone focused non-traded REIT. Tools and data for analyzing Skybridge’s fund of hedge funds products, visit www.tenderofferfunds.com. For data on Skybridge’s non-traded REIT, as well as other private real estate funds, visit our tools and data section. Additional information on SkyBridge including offering documents, are available at www.skybridge.com