Redemption overload at Blackstone’s flagship non-traded REIT cast a pall over the whole retail alternative sector for several months. Blackstone had to delay the launch of Blackstone Private Equity Strategies Fund(BXPE), a publicly registered vehicle designed to bring traditional private equity to a wider audience of investors.

Yet the launch plans are back on now, as the Financial Times has reported. Blackstone will begin taking subscriptions from investors in Q4 of this year, and the fund will officially launch in January 2024.

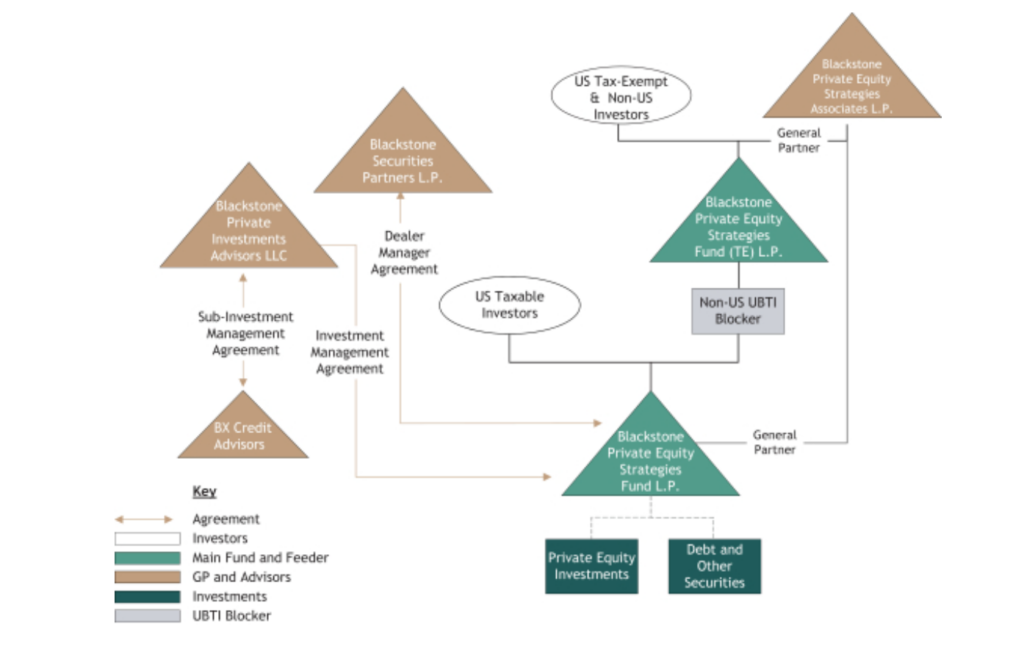

A closer look at Blackstone Private Equity Strategies Fund

According to public SEC filings, BXPE will conduct a private offering to investors that qualify as both accredited investors and qualified purchasers. It is a perpetual life strategy with monthly fully funded subscriptions and periodic repurchase offers. Theoretically this structure will be optimal for investors looking to include a targeted percentage of private equity exposure as part of an overall allocation strategy or model portfolio.

BXPE will receive a management fee of 1.25% of NAV, plus a performance allocation of 12.5% over a 5.0% hurdle.

BXPE also plans to offer to repurchase 5% of units per quarter, although these repurchase are at the discretion of the GP. This is a similar setup to the NT REITs and BDCs, where repurchases are at the discretion of the board.

BXPE will file quarterly reports on form 10-Q, and annual reports on Form 10-K. This will provide more transparency than typical for a private equity fund, although the underlying portfolio holdings will still be private.

Here is the fund’s strategy:

Implications of BXPE’s Revival

So Blackstone Private Equity Strategies Fund is back on. Does this mean the redemption storm has passed? No, there will always be liquidity mismatches in investment funds that hold illiquid assets but have an investor base expecting more frequent liquidity. However, if advisors manage client expectations, and make realistic liquidity plans, then alternatives will still play a valuable role in retail investor portfolios. Blackstone’s plan to move forward with BXPE is a bright sign for this sector.

This post is part 2 of a 2 part series. Click here to read the first post.

Managing the tradeoff between liquidity and performance is a central challenge for allocators and investment professionals. Building a Better Portfolio: Balancing Performance & Liquidity is a great resource for allocators and investors looking to systematically meet this challenge. In a previous post we summarized the five components of an asset allocation model that incorporates private market assets. In this post we’ll discuss a few more highlights from the paper.

A good private asset commitment strategy must balance several investment objectives. These include performance, risk and liquidity. Over the years academics and practitioners have developed a variety of models and heuristics to balance these objectives.

In How Large Should Your Commitment to Private Equity Really Be? Researchers propose a simple rule of thumb. Simply commit the capital allocated to private assets each year. This is a deterministic rule, and it does not make use of any currently available information. The goal is to build and maintain a desired allocation to the targeted asset class. Other possible methods include basing the allocation decision on the amount of uncalled capital, cash, NAV and recent distributions. The idea is to consistently commit a fraction of overall capital.

Another slightly more advanced framework is known as the Nevins commitment model.

Nevins Commitment Model

The Nevins Commitment model comes from a paper in the Journal of Alternative Investments: A Portfolio Management Approach to Determining Private Equity Commitments.

This model uses four parameters.

Rate of capital calls

Rate of Distribution

Rate of Return on Public Assets

Rate of Return on private assets

Since it requires input from external data sources, its a bit more advanced than simple rules of thumb. Nonetheless, it is much simpler to implement than more complex allocation models.

Three important questions for private asset investors

An asset allocator that makes commitments to private assets needs to balance many competing demands. As they build their process, they should always keep three questions in mind:

How to formulate a private asset commitment strategy to manage private asset exposure and the uncertainty in timing and magnitude of their cash flows over time?

What should be the desired allocations (public vs. private, public passive vs. public active) given the investor’s liquidity risk tolerance?

How would various market scenarios impact the portfolio’s liquidity and performance?

Click here to read the GIC and PGIM paper that develops a framework for answering these questions.

Running Cash Flow Simulations

Best practices for allocators involve running simulations to see how various commitment strategies impact cash flows. By stress testing “:worst case scenarios” an investor can position the portfolio in a way that avoids a situation where they are forced to sell good assets at a discount to meet liquidity demands, while still allocating enough to illiquid assets to achieve desired returns.

Alternative investments are an important part of any asset allocation strategy. Used wisely, they can enhance returns and reduce risk. A key part of using alternative investments wisely involves balancing the tradeoff between liquidity and performance.

See also: Closed end interval funds are a fund structure designed to force an elegant compromise between two extremes of liquidity structures. This fund structure can be used for a wide variety of strategies, and is becoming increasingly popular with both mass affluent and institutional investors.

Traditional portfolio management techniques such as mean-variance optimization or risk parity don’t capture the reality faced by an allocator building a portfolio that includes alternative investments. These traditional methods focus on return variability and drawdowns, while treating liquidity risk as a secondary considerations.

Yet in reality, liquidity risk is of critical importance. In fact, while return variability and drawdowns are generally transitory, liquidity risk can cause permanent damage to a portfolio.

There is a tradeoff between performance and liquidity in asset allocation. At one extreme, holding illiquid but high performing assets might give investors little room to maneuver and meet liquidity demands. In a downside scenario, these illiquid assets would ultimately hurt performance because the allocator would need to sell them prematurely at a discount to meet cash needs. At the other extreme, an all liquid portfolio might not generate the high enough returns. Handling this tradeoff is the central challenge for allocators and alternative investment professionals.

GIC and PGIM produced a joint research paper that develops a framework for systematically handling this tradeoff. The paper develops a cash flow-driven asset allocation framework to help investors formulate private asset commitment strategies, determined desired allocations to private funds, and understand how various market scenarios would impact liquidity and performance of their portfolio.

Most research in this area generally falls into two buckets: cash flow prediction models, and private asset commitment strategies. GIC and PGIM integrate these strategies.

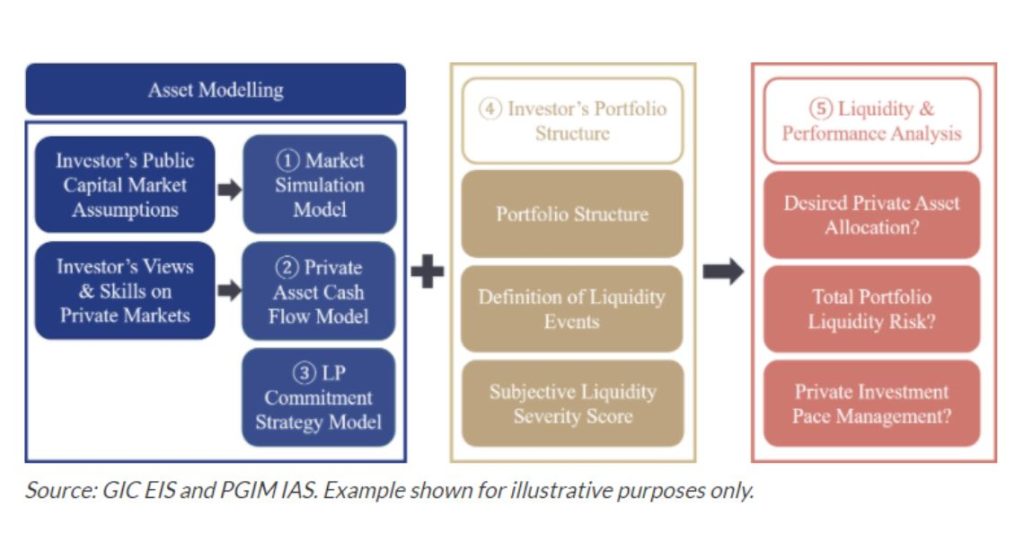

Visualizing the role of private investments

This flow chart explains the framework for allocating to private investments.

This asset allocation framework has five major components

Market simulation model

Private Asset Cash Flow Model

LP Commitment Strategy Model

Investor’s Portfolio Structure

Liquidity and Performance Analysis

The first three steps involve asset modelling. To begin with the researchers simulated the risk and returns of a multi-asset portfolio, including private and public markets. They used the Takahashi and Alexander Model to capture empirical relations between cash flows and public market performance. This framework is also flexible, because it allows investors to input their own public capital market assumptions. This is the first step in the framework- the Market Simulation Model.

The second step, Private Asset Cash Flow Model is closely related to the first step. The framework allows the investors to input their views on private markets and estimate their skills and how they might impact expected returns. A cash flow model that is responsive to underlying capital market conditions allows an allocator to perform stress tests, and tailor liquidity analysis to their estimates for future market scenarios.

The third step involves applying an LP commitment strategy. There are two options. The first is a Cash flow Matching strategy. This involves building a private asset portfolio whose periodic net cash flows are close to zero. So distributions received in each quarter should fund capital calls in the next quarter. A benefit of this strategy is the fact that it can insulate the rest of the portfolio(ie the publicly traded portfolio), from private asset investment activity. This strategy also has limitations In particular it leads to volatile commitment patterns, and since it may result in skipping commitments over multiple periods can make it hard to diversify by fund vintage. Additionally the strategy has no control over how NAV will grow as a percent of overall portfolio. This strategy is also not possible if an allocator is starting a new private capital investment program from scratch, it can only make commitments once distributions have started to arrive.

The second LP commitment strategy is called Target NAV. With this strategy the allocator tries to achieve target NAV as a percentage of the overall portfolio. This strategy divides the private portfolio into three pools of capital- (1) “in the ground” asset also known as the NAV, (2) Committed but uncalled capital, and (3) uncommited capital which is to be allocated to private assets, and distributions from prior commitments that have not yet been committed to new commitments. An advantage of this strategy is that it treats the private allocation of a self contained portfolio. A drawback of this strategy is that it doesn’t balance cash flows, and might require frequent interactions with other parts of the portfolio in order to absorb or free up capital for private market related cash flows.

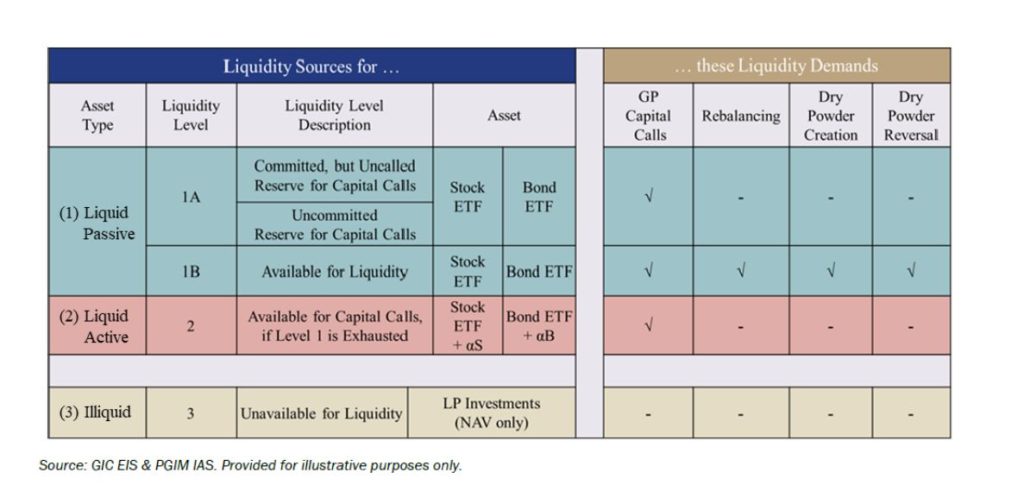

The fourth component of the asset allocation framework is Portfolio Structure. The framework sorts assets by transactability- that is the ease and cost of selling. There are three types of investments, two liquid, and one illiquid. Liquid investments include Liquid passive and liquid active, which are actively managed inpursuit of alpha. . The third category is simply private market investments. This diagram shows how there is a “waterfall” for sourcing liquidity:

A liquidity event occurs whenever an investor needs to move down the waterfall to find lqiudiity. A large liquidity demand could produce a cascade.

The fifth component of the asset allocation framework is Liquidity and Performance analysis. There are four categories of liquidity demands. Quoting from the paper:

GP Capital Calls: An obligation that an LP must fulfill based on total initial committed capital amounts, but the timing and amount of each capital call are not under the LP’s control;

Rebalancing: Shift portfolio allocation between public stocks and public bonds at quarter ends to maintain policy or target weights;

Dry Powder Creation: A tactical move into higher beta assets (i.e., stocks) during market downturns (i.e., at the end of each month if the public equity market experiences a large drawdown) to provide market support or to take advantage of the market dislocation;

Dry Powder Reversal: When a market recovery occurs (i.e., when a drawdown is less than -5% following a recovery in the equity market) there is a need to adjust public stocks and bonds back to their initial relative target weights.

The paper also has a case study that illustrates how commitments strategy and portfolio structure interact to determine expected performance. Click here to access the research paper.

In a subsequent post, we’ll follow up with more on portfolio construction with illiquid private assets.